Cortex Advisory Research Note #2: Semiconductors Will Grow 90% This Year; Half the iIndustry is Still at the Bottom

WSTS puts the 2026 market at a record $1.51 trillion. The number is right — and it will mislead you, because it sums two industries moving in opposite directions.

The most misleading semiconductor number of 2026 might be the total itself.

The World Semiconductor Trade Statistics (WSTS) group projects the global market to be up to $1.51 trillion this year, up nearly 90%, with the memory segment growing close to threefold. For context, 2025 sales were $791.7B, up 25.6% — so the market is set to nearly double in a single year. Look only at that, and everyone reaches the same conclusion: a broad, industry-wide recovery has arrived.

Split the total open, though, and you find almost the opposite story.

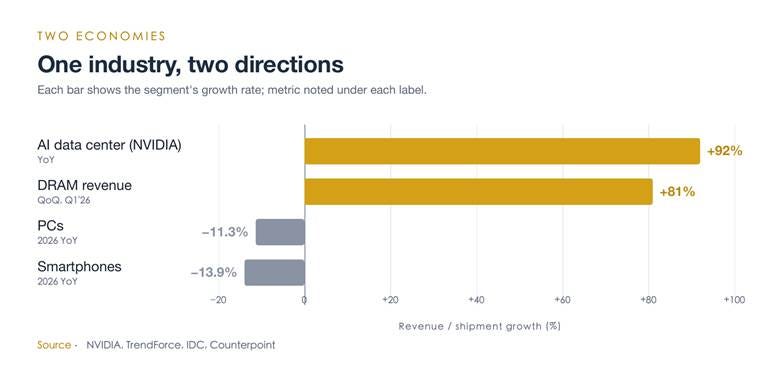

Nearly all of the growth comes from one narrow band: AI accelerators, high-bandwidth memory (HBM), advanced nodes, and advanced packaging. In Q1 2026, DRAM industry revenue alone rose 81% sequentially; NVIDIA’s data-center segment hit $75.2B in a single quarter, up 92% year-on-year. Do the math, and AI plus data center absorbed nearly half of this year’s entire revenue increase. Inside the band, it’s a textbook seller’s market: sold out, record margins, customers queuing to sign long-term contracts just to lock supply.

In the same year, global smartphone shipments are forecast to fall 13.9% and PCs about 11.3% — the flip side of the AI boom is a still-shrinking consumer chain.

Outside the band, the climate is entirely different.

Mature nodes — the older processes that automotive, industrial, and consumer chips run on — mostly aren’t expected to bottom until 2026. Taiwan’s UMC, VIS, and PSMC raised prices on some products by up to 10% from April, which looks like a recovery, but elevated inventory plus persistent low-price competition from Chinese capacity has capped any broad rebound. A real recovery in automotive silicon isn’t expected before 2027. On the consumer side, the numbers are blunter: smartphones are tracking down 13.9% this year, PCs about 11.3%. Under one “semiconductor” banner, one half can’t get enough supply, and the other can’t move it.

So, semiconductors in 2026 are less one industry than two economies.

One is the AI narrow band: short of supply, raising prices, earning the highest margins in its history, with pricing power firmly on the sell side. The other is the mature chain: inventory not yet cleared, prices pressed by Chinese capacity, recovery patchy rather than broad. They share a name, but their position in the cycle, their pricing power, and their customer structure are nearly opposite. Add the two and divide by two, and the “average temperature” describes neither — like putting a feverish patient and a hypothermic one on the same chart and calling the mean normal.

It also explains a dissonance a lot of people feel but can’t quite name: why their own read of 2026 keeps clashing with the headlines. The answer is simple — it depends on which side of the line you’re on. If your company sits in the AI band, you’re living the best year on record; if you’re in the mature chain, you’re living a year still waiting for the floor while watching rivals cut prices.

And once the temperature gap inside an industry gets this wide, “how’s the chip cycle doing” stops yielding a useful answer. Worse, it hides the real risks: the dazzling total masks both the bleeding in the mature chain and the boom’s heavy dependence on a tiny set of buyers — when nearly half the AI increment comes from data centers, concentrated in a handful of cloud giants, the band’s prosperity rests on a very narrow fulcrum.

So the question to ask about 2026 was never “Is the cycle good?” It’s two sharper ones: will the AI band widen and pull the mature chain up with it? Or stay narrow — even narrower — and let the gap between the two economies keep stretching? Where capital, capacity, and talent flow will answer that sooner than any forecast — and right now they’re flowing almost entirely one way. For any chip company, knowing which side of the line you’re on matters far more than the $1.5-trillion total.

Adapted from Cortex Advisory’s Global Semiconductor Industry — H1 2026 Deep Dive. Cortex Advisory is an independent strategy research firm focused on semiconductors and AI infrastructure supply chains.

More research & deep dives → cortex-advisory.com

About Cortex Advisory:

SOURCES

WSTS, Global Semiconductor Market Forecast 2026 — https://www.wsts.org/76/103/Global-Semiconductor-Market-Surges-Beyond-15T-2026

SIA, 2025 global semiconductor sales $791.7B, +25.6% — https://www.semiconductors.org/global-annual-semiconductor-sales-increase-25-6-to-791-7-billion-in-2025/

TrendForce, Q1 2026 DRAM industry revenue +81% QoQ — https://www.trendforce.com/presscenter/news/20260601-13070.html

NVIDIA FY27 Q1 results (data-center revenue $75.2B, +92%) — https://nvidianews.nvidia.com/news/nvidia-announces-financial-results-for-first-quarter-fiscal-2027

TrendForce, mature-node bottom 2026, Taiwan price hikes from April — https://www.trendforce.com/news/2026/04/03/news-mature-node-prices-may-rebound-in-2026-but-inventory-overhang-and-china-competition-weigh/

IDC, 2026 global smartphone shipment forecast -13.9% — https://www.fonearena.com/blog/480087/global-smartphone-shipments-q1-2026-idc.html

Counterpoint, 2026 global PC shipment forecast — https://counterpointresearch.com/en/insights/global-pc-shipments-q1-2026

(This piece reflects the author's opinion, and does not represent the opinion of TechSoda.)

| A guest post by

|